Managing multiple debts can be overwhelming, especially when each account comes with its own interest rate, minimum payment, and due date. Not only does this juggling act increase the risk of missed payments and late fees, but it also makes tracking your financial progress challenging. Over time, the burden of coordinating several payments can take a toll on your emotional well-being, leading to stress and anxiety about your financial future. Debt consolidation is a financial strategy designed to make your debt more manageable by combining all your existing debts—such as credit cards, personal loans, or medical bills—into one new loan, frequently at a lower interest rate

Lenders like Symple Lending specialize in providing tools and options that allow borrowers to consolidate their debts efficiently. These lenders typically offer personalized solutions that fit your unique financial situation, helping you tailor a repayment plan that works within your budget. With a consolidated loan, you’ll pay a single monthly bill instead of juggling several, simplifying your financial life significantly. This not only reduces administrative hassle but also minimizes the risk of missed payments or confusion over which account is due when. For many borrowers, consolidating debt offers a more straightforward path toward becoming debt-free. It can free up more funds in your monthly budget for other essential needs, such as savings, emergency funds, or even the occasional treat to reward your progress.

Table of Contents

Benefits of Debt Consolidation

Lower Interest Rates

By consolidating high-interest debt—such as credit cards—into a loan with a lower rate, you can pay considerably less in interest over the long term. Debt consolidation loans or balance transfer offers can sometimes cut your interest rate by half or more, saving you hundreds or even thousands of dollars. This means more of your monthly payment goes directly toward reducing your principal balance, speeding up your journey to financial freedom and allowing you to create a solid timeline for becoming debt-free.

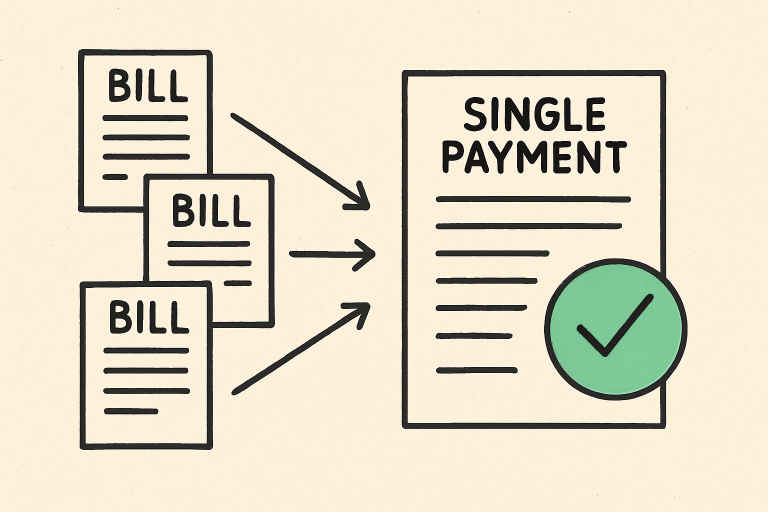

Simplified Payments

It can be challenging to keep track of multiple due dates and amounts, especially if your debt is spread across many accounts. A single payment each month makes the process easier, reducing the risk of missing payments and incurring late fees, which can further exacerbate your debt problems. This simplification can give you peace of mind, freeing up mental energy for other priorities in your life.

Fixed Repayment Schedule

Most debt consolidation loans come with set terms and consistent monthly payments. This provides you with a precise payoff date and takes much of the guesswork out of your financial planning. Knowing exactly how much you owe each month and when your debt will be paid off allows you to budget more effectively and can boost your motivation as you watch your balance steadily decrease.

Also Read

Potential Drawbacks

More extended Repayment Period

Consolidating your debt may lower your monthly payments, but it might also mean extending your overall repayment period. While the monthly savings can be helpful, you could end up paying more interest over the life of the loan, particularly if you select a longer repayment term. Carefully consider your goals; sometimes, a slightly higher payment in the short term leads to greater savings down the road.

Fees and Costs

Some debt consolidation loans include origination fees, balance transfer fees, or prepayment penalties that can cut into any potential savings. For example, a loan might come with an upfront fee based on a percentage of your balance, or transfer offers may only provide a temporary low interest rate before reverting to a higher rate. Always review the terms carefully before committing so you fully understand all potential costs.

Risk of Accumulating More Debt

If you don’t address the habits or circumstances that led to your original debt accumulation, there’s a risk of falling into the same patterns. It’s important to use debt consolidation as part of a larger plan to improve financial discipline, such as tracking expenses, reducing unnecessary purchases, and building up an emergency fund to help you avoid relying on credit in the future.

After you have consolidated your debts, you might benefit from professional advice to ensure you stay on track and avoid reverting to old spending habits. Working with debt consolidation experts can provide personalized guidance and help you build a sustainable strategy for long-term financial health. These professionals often offer budgeting tips, debt management strategies, and emotional support, which can be invaluable during your journey to financial stability.

Is Debt Consolidation Right for You?

Debt consolidation is not a one-size-fits-all solution, and it’s crucial to look at your unique financial situation before making a decision. You should take a close look at your income, total debt load, credit score, and future expenses, since these factors will influence the terms you can receive and the amount you can save. If consolidating your debt results in a lower interest rate and affordable monthly payments, it can be an excellent step toward getting ahead financially. However, if the new payment is still unaffordable, or if it encourages you to keep spending, the benefits may be outweighed by new risks.

It’s wise to review your budget and consider alternatives before moving ahead. According to NerdWallet, checking your eligibility for lower rates, understanding all associated fees, and honestly assessing your ability to stick to a repayment plan are vital factors in deciding whether consolidation will work for you. Being realistic about your own habits and circumstances is an essential first step toward a successful debt management or repayment plan.

Alternative Strategies

Debt Snowball Method

Pay off your smallest debts first, regardless of the interest rate, to quickly eliminate accounts and build motivation as you see your balances disappear. This psychological boost can help you stay committed to your repayment journey, even when it feels difficult.

Debt Avalanche Method

Target debts with the highest interest rates first. This approach saves money on interest but may take longer to pay off the initial debt, requiring more patience and persistence. Over time, focusing on the most expensive debts first ensures you’re using your resources most efficiently.

Credit Counseling

Seek help from a nonprofit credit counseling agency or a certified financial advisor. They can help you build a custom repayment plan or negotiate with creditors for better rates or terms. These services can be especially useful if you’re struggling to make minimum payments or need help building a realistic budget.

Exploring all your options ensures you choose the path that best supports your long-term financial security.

Conclusion

Debt consolidation offers a practical solution for managing overwhelming debt and reducing monthly financial strain. Before proceeding, weigh the benefits against the drawbacks, consider your financial habits, and explore all available options. With careful planning and perhaps the support of financial professionals, you can use debt consolidation to regain control of your finances and work toward a more secure, debt-free future. Taking action now could help you resist further temptation and build the foundation for a life free from the constant stress of debt.